TEMPE Zero Down Bankruptcy Attorneys

I know what you’re thinking… Is This Really a $0 Down Bankruptcy Filing?

We have handled Arizona Bankruptcy for over a decade. Our Tempe bankruptcy lawyers offer sound guidance for individuals and small businesses who are devastated by unpaid debts and other financial obstacles. Therefore, the first step toward finding a solution to your financial troubles is contacting My AZ Lawyers and discussing your situation with a Tempe bankruptcy lawyer.

Call (602) 568-7410 now to make sure to qualify.

Do you need financing?

Instant Approval Available Apply Now

How Our Top Rated TEMPE Bankruptcy Lawyers Can Help You

Have you experienced an unexpected illness or injury? Lost your job? Gone through an expensive divorce? Or do you simply have credit cards and other debts that have gotten out of control? You don’t have to continue the cycle- debt relief is available. The seasoned professionals at My AZ Lawyers are standing by to walk you through these options, and provide bankruptcy representation if that is the best option for you. Our consultations are free of charge, and our representation fees are reasonable and fair.

Bankruptcy is a federal program that can be relatively short compared to other legal matters. However, it can also be complex, and the consequences of an incorrectly filed petition can be severe. That’s why it’s best to proceed with guidance from an experienced bankruptcy attorney.

Our bankruptcy lawyers have seen it all, and have no judgment for our clients. We will help you discharge unsecured debts like judgments, credit cards, and medical bills, and keep as many of your assets as possible.

In some situations, a reorganization bankruptcy may provide you more relief than a liquidation bankruptcy. This can significantly reduce the amount you pay in interest, as well as protect you from your creditors for several years in the meantime. But you don’t have to make this decision alone. Our Tempe bankruptcy attorneys are here to help you decide which form of debt relief will best suit your needs.

Additionally, even good people can fall behind. For example, even the most responsible people can run into trouble financially. Therefore, bankruptcy provides the option for debt relief that some people need. Given these points, consider Tempe bankruptcy services when facing the possibility of declaring bankruptcy in Tempe.

In particular, our Tempe bankruptcy attorneys have the experience and knowledge that will benefit you greatly. Consider hiring our low cost bankruptcy services Tempe. Call us now at (602) 568-7410 for a free consultation either by phone or in our downtown Tempe bankruptcy office. Bankruptcy Services Tempe, we strive to make you debt free.

Tempe Bankruptcy Services

What Is It? Bankruptcy Code Explained

Arizona bankruptcy laws offer certain protections to debtors who are needing to eliminate debt through reorganization or liquidation. Thus, the bankruptcy code, called Title 11 of the United States Code, details these procedures. Furthermore, the bankruptcy code is a uniform federal law that oversees all bankruptcy cases. In addition, it has been amended several times since it’s original completion. In fact, the filing of most bankruptcies in the bankruptcy code fall under Chapter 7, Chapter 11, and Chapter 13.

What types of bankruptcy can I file as a consumer?

Chapter 7 Bankruptcy in Tempe:

This is the most popular type of bankruptcy. This could possibly be because it liquidates and discharges most types of unsecured debts. However, assets that aren’t protected by state exemptions can be seized and sold to pay debts. Your bankruptcy petition will need to include information about all of these areas so that the court can analyze and determine if you should be allowed to discharge your debts through Chapter 7 bankruptcy.

Chapter 13 Bankruptcy in Tempe:

This type of bankruptcy, which also is referred to as a wage earner’s bankruptcy, reorganizes debts into a payment plan. Many debts must be paid in full in the plan, but some unsecured debts can be discharged with only minimal repayment. Debtors aren’t restricted by the same income limits and asset exemptions as they would be in a Chapter 7 bankruptcy. Depending on how the debtor’s income compares to the state median, their payment plan will last 3 or 5 years.

Chapter 11 Bankruptcy in Tempe:

This type of bankruptcy is typically only used by businesses and individuals with extremely high income, assets, and debts. In Chapter 11 bankruptcy, the debtor’s top creditors will join to form a creditor committee which will have authority over major financial decisions, as well as voting approval on the debtor’s proposed plan to emerge from debt. It allows a business to continue operating, where it would be forced to close in other chapters.

Discount Bankruptcy Services Tempe

Time is of the essence when deciding if you should file for bankruptcy. Many of your financial situations are already dire and pressing, there is no time to waste when you have made the decision to do something effective about it. Thus, our Tempe bankruptcy lawyers from our Tempe bankruptcy law firm can assist you in determining how to resolve your financial situation and protect your rights through affordable debt relief. Isn’t it time for a fresh start? The Tempe bankruptcy lawyers from My AZ Lawyers can provide you a new start at a fraction of the cost of other Tempe attorneys.

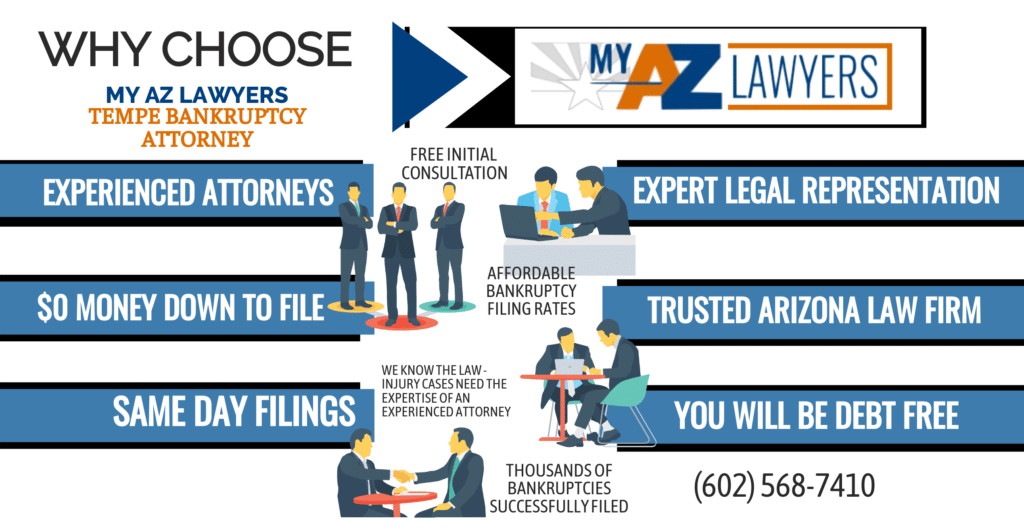

My AZ Lawyers Bankruptcy Attorney Can Help – Best Debt Relief Options

Working with a My AZ Lawyer bankruptcy attorney can help you determine which option will be best for you to get the debt relief you need while also protecting your assets. In addition, filing for bankruptcy is a complex process, and it is easy to make a mistake with the documentation if you attempt to handle it yourself or to use a document service. In particular, a Tempe lawyer can help you file the paperwork properly and to help you find all the opportunities to get the best debt management plan for your circumstances.

As a result, you should stop feeling like your financial circumstances are beyond your control. If you are struggling with debt, speak with My AZ Lawyers today for the best debt relief options in Tempe. The bankruptcy services Tempe can help. Call (602) 568-7410 for a FREE consultation.

Awards &

Associations

ARIZONA BANKRUPTCY CODE

Understanding bankruptcy is an important step to determining if bankruptcy is the right choice to eliminate your debt, and it can help you decide which chapter to file. For example, when individuals or businesses owe more debt than they can pay, bankruptcy laws and rules assist with debt relief. The filing of bankruptcy cases occurs in a bankruptcy court; a federal court. In addition, the federal laws that govern bankruptcy cases allow for debtors to liquidate assets to pay debt, or create a repayment plan to reorganize debt and pay back creditors over time.

HOW IS IT POSSIBLE TO FILE BANKRUPTCY WITH Zero $ Down?

Not only can you pay for your bankruptcy after filing, but you can do so at a 0% interest rate, and your plan includes credit reporting. This means that every payment you make towards your bankruptcy will help you improve your credit score after your debts have been discharged.

If you are in an emergency situation, our attorneys offer same day filings. This could be an impending garnishment, repossession, foreclosure, etc. We will get you filed quickly and correctly so that you can keep your assets and move forward with a clean financial slate.

TEMPE CHAPTER 7 BANKRUPTCY LAWYERS

Chapter 7 bankruptcy is the most common bankruptcy filing in Tempe. Another key point, Arizona Chapter 7 bankruptcy protection allows debtors to keep exempt and essential assets while eliminating dischargeable debt. Also, a bankruptcy means test indicates who is eligible to file Chapter 7. Our experienced Chapter 7 bankruptcy attorneys can help you get out of debt.

$0 DOWN BANKRUPTCY IN TEMPE, ARIZONA

Considering filing bankruptcy? Call us about the zero down bankruptcy program. Especially, if your decision includes needing a bankruptcy attorney, but you don’t know how to pay the legal fees up front (which bankruptcy filing requires). Also, if you cannot afford to pay legal fees up front, be sure to call our Tempe Bankruptcy Lawyers (602) 568-7410find out if you qualify for the $0 down program.

TEMPE CHAPTER 13 BANKRUPTCY ATTORNEY

Bankruptcy Courts in Arizona

A United States bankruptcy judge presides over the bankruptcy cases. This judge has the power to make decisions over all matters concerning federal bankruptcy cases. For each judicial district in Arizona, there is a bankruptcy court. In Arizona, the bankruptcy courts are located in:

Tucson

US BANKRUPTCY

COURT

38 S Scott Ave,

Suite #900-6A

Tucson, AZ 85701

Yuma

US BANKRUPTCY

COURT

98 West 1st Street,

2nd Floor,

Yuma, AZ 85364

Flagstaff

US MAGISTRATE

COURTROOM

123 North

San Francisco Street,

Flagstaff, AZ 86001

Bullhead City

MOHAVE COUNTY

SUPERIOR COURT

2225 Trane Road,

Courtroom R,

Bullhead City, AZ 86442

WHAT YOU SHOULD KNOW ABOUT THE CREDIT COUNSELING REQUIREMENT IN TEMPE

Many people don’t realize that they are required to complete credit counseling in order to discharge their debts in bankruptcy. These courses can be completed online, and generally take about 1-2 hours. You will also need to discuss your situation with a credit counselor. You must include a course completion certificate with your bankruptcy petition, or else your case could be dismissed.

TEMPE BANKRUPTCY LAWYERS

Payment Plan Options to file Bankruptcy in TEMPE – File Now Pay Later!

Contact An Experienced Bankruptcy Attorney Today

Therefore, when you need to stop a wage garnishment, end harassing phone calls from creditors, or even stop a foreclosure, you need an experienced attorney to take action immediately. My Arizona Lawyers offers a $0 Down Bankruptcy program, so filing for bankruptcy requires zero money out of pocket. You pay zero money to wipe out debt. In other words, zero money takes back control of your life. Also, Zero money down to stop the phone calls from creditors. Zero money down to end a Tempe wage garnishment. Plus, Zero money down to retain a Tempe bankruptcy attorney who is dedicated to protecting your rights as a debtor. Bottom line – zero money down gets you out of debt!

Disputes And Litigation In The Bankruptcy Court

Skilled TEMPE Bankruptcy Attorneys Representing You In Court

When a bankruptcy petition is filed, creditors listed on the paperwork receive a notice from the court that a bankruptcy was filed by the debtor. Also, when a bankruptcy involves liquidation of property and assets, there may not be much money available to pay creditors. In these cases, normally the debtor is given a bankruptcy discharge. Therefore, if a discharge is granted, a debtor is no longer personally liable for repaying debt. Thus, it is possible for disputes to arise, and in some cases, litigation in the bankruptcy court – proceedings, settlement efforts, or a trial is necessary.

TEMPE Bankruptcy Myths Uncovered

Myths and Truths Regarding Bankruptcy in TEMPE, Arizona

The Tempe Bankruptcy Attorneys at My Arizona Lawyers realize that there are a myriad of reasons that people have to file for bankruptcy protection in Tempe. Therefore, the process of declaring bankruptcy in Maricopa County is complex. This is made even more difficult with the many myths and fallacies out there. In the following, our knowledgeable Maricopa County Bankruptcy Attorneys dispel common bankruptcy myths. Our Tempe debt relief lawyers tirelessly work to help individuals, couples, families, and businesses in Maricopa County file for bankruptcy protection.

Common Fallacies About Filing for Bankruptcy

Filing for Chapter 7 bankruptcy in TEMPE, Arizona

The primary purpose of a Chapter 7 bankruptcy is to eliminate certain kinds of debt. The bankruptcy court must receive a case filing and administrative fees in order to file a bankruptcy petition. Next, a filer must complete official bankruptcy forms. These forms include the petition to file, schedules, and statement of debt/financial affairs. The filer should also include and provide the following paperwork:

One of the schedules the filer must file is that of exempt property. According to the Bankruptcy Code, some property is protected, or exempt, from creditors. However, Arizona has adopted its own exemption law. Filing a bankruptcy petition under Chapter 7 puts the automatic stay into effect immediately. The stay is effective to protect a debtor from collection activity from a creditor. Furthermore, the bankruptcy court appoints a trustee to administer the bankruptcy case, and to carry out the liquidation of the non-exempt assets.

Because of the complexity of the Bankruptcy Code, it is wise to consult with an attorney who can evaluate your debt, listen to your needs, and look at your property/assets.

CHAPTER 7 – BANKRUPTCY

Chapter 7 is the most popular form of consumer bankruptcy, and it’s no wonder why. Chapter 7 allows you to discharge most types of unsecured debt, even if you have some income and property. You can qualify either by making less than Arizona’s state median income for your household size, or by passing the Means Test. Our Tempe bankruptcy lawyers will help you make sure that you qualify, and that Chapter 7 bankruptcy is the best fit for your needs.

CHAPTER 7 – LIQUIDATION BANKRUPTCY

The Chapter 7 bankruptcy process typically takes about 4 to 6 months from filing to discharge. In this time, you will clear away personal loans, credit card debt, medical bills, repossession deficiencies, unpaid utilities, some taxes, and more. You will also be able to keep any property that is protected by state exemptions. However, some forms of unsecured debts can’t be discharged in bankruptcy, like domestic obligations and most student loans. To see if you qualify, and whether your debts are dischargeable, call or use our online form for your free consultation with one of our Tempe bankruptcy attorneys.

CHAPTER 7 – BANKRUPTCY DISCHARGE

A Chapter 7 bankruptcy discharge can be granted in a few months after filing the petition. A bankruptcy discharge is a permanent order stating the debtor is no longer legally required to pay back debt listed in the case. Therefore, a discharge prohibits a creditor from taking action to collect on any debts that were eliminated in the bankruptcy. In addition, a creditor may not communicate in any way or take legal action to collect debt. The discharge is given in Chapter 7 cases approximately four months after the date of the petition filing. There is also an amount of time where a creditor can object to the discharge, and when this period ends without a motion to dismiss the case, the discharge is granted.

Additionally, a discharge is not automatically granted just because the process is completed. A creditor, a trustee may file an objection. Meaning, a creditor may file a complaint before a deadline date. The bankruptcy code describes the reasons a discharge may be denied. For example, not providing the proper documentation, failure to complete the required credit counseling / financial management course, or covering up property with intent to defraud. A Chapter 13 bankruptcy case is a bit different. Normally the debtor is entitled a discharge when the payments under the plan are completed.

Bankruptcy Petition And Automatic Stay

A bankruptcy case either involves liquidation of property, or establishes a plan to repay creditors. Typically, to begin a case, the debtor files a petition with the bankruptcy court. Statements are also filed that list liabilities, income, assets, the name(s) of creditor(s), and the amount of debt owed. One of the provisions of the bankruptcy law is the automatic stay. Thus, upon filing of a petition, all debt collection attempts must stop. Filing bankruptcy “stays,” or prevents debt collection actions by creditors for payment or property. Therefore, when the automatic stay is in effect, a creditor may not garnish wages, bring about or continue a lawsuit, or contact the debtor. This includes phone calls demanding payment or making harassing threats to get a payment.

Filing a bankruptcy petition puts the Automatic Stay into effect. This means you have the protection of the bankruptcy court as soon as your case is filed. Why is this important?

The Automatic Stay prevents any creditor from collecting on a debt:

- No collection attempts

- No phone calls from creditors

- Wage garnishment stops

- Lawsuits

- Stop a foreclosure

Because the Automatic Stay begins the moment the bankruptcy is filed, our Tempe Bankruptcy Lawyers understand that for some clients, an immediate filing is crucial. That’s why My Arizona Lawyers offers a $0 down bankruptcy program as well as payment plan options. We make eliminating debt through bankruptcy affordable and possible for debtors needing the bankruptcy protection of the Automatic Stay.

CLIENT REVIEWS & TESTIMONIALS

Natasha Lenard

🟊🟊🟊🟊🟊

Adam Walsh

🟊🟊🟊🟊🟊

Alexandra Ortiz

🟊🟊🟊🟊🟊

5 Bankruptcy Warning Signs That Could Be Exacerbated by Holiday Spending

Struggling with holiday debt? Learn how filing bankruptcy in Arizona can help clear debt and regain control, especially when holiday spending causes stress

TEMPE BANKRUPTCY FAQs

Our experienced Tempe Bankruptcy Attorneys answer some of the most asked questions regarding Chapter 7, Chapter 13, and Emergency Bankruptcy filings. Also, our Tempe Debt Relief Team also looks at questions regarding: Wage Garnishments, Repossessions, Foreclosures, and Medical Bankruptcies. Read on, get important information for anyone considering declaring bankruptcy in Tempe, AZ.