GILBERT Bankruptcy ATTORNEYS

Debt Relief – Zero Down Gilbert Bankruptcy Lawyers – Bankruptcy Attorneys in Gilbert, Arizona

Chapter 7

Bankruptcy ATTORNEYS

add text here

Chapter 13

Bankruptcy ATTORNEYS

add text here

GILBERT ZERO DOWN

Bankruptcy FILING

add text here

CHAPTER 7 BANKRUPTCY FAQs

Frequently Asked Questions About Chapter 7 Bankruptcy

Our Gilbert Chapter 7 Bankruptcy Lawyers answer frequently asked questions regarding Chapter 7 bankruptcy, filing for bankruptcy protection in Gilbert, Arizona, and seeking debt relief assistance in Gilbert.

As the coronavirus pandemic continues to impact people in Gilbert, Maricopa County, and throughout Arizona; with no end in sight, more and more people rely on credit cards and other forms of personal debt to make ends meet. Unemployment rates in Arizona have reached rates unseen since the Great Depression. Therefore, with millions of American families relying on unemployment assistance and stimulus checks provided by the CARES Act. Some of these people may have not previously qualified for Chapter 7 bankruptcy, but now do due to a sharp decrease in income. Once CARES Act benefits, as well as eviction moratoriums, and other protections meant to mitigate the pandemic’s effects, expire, bankruptcy may be a viable option for people in Gilbert and throughout Arizona. For additional information, call our Gilbert bankruptcy office today at (602) 598-5099.

ANSWER:

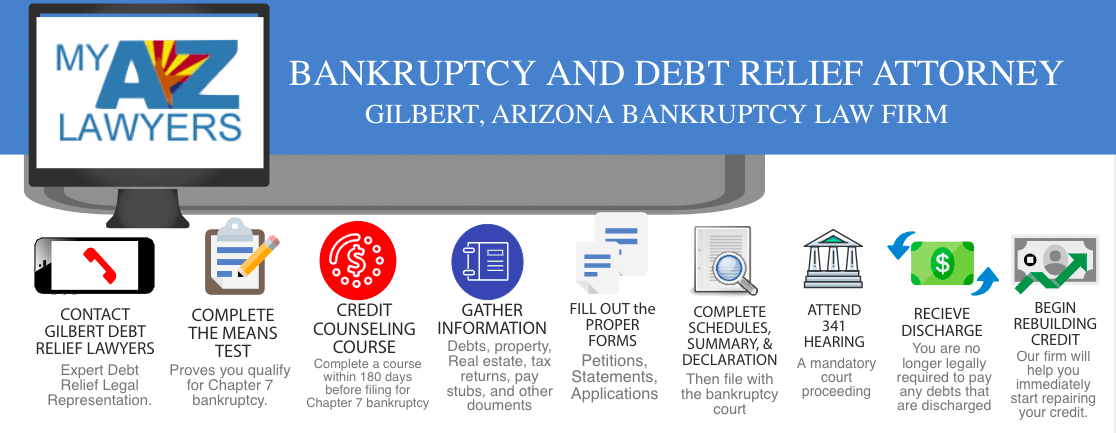

It is a common misconception that anyone who has a job only has Chapter 13, also known as a wage earner’s bankruptcy, available to them. However, there are two methods to qualify for Chapter 7 based on income: through the state median income level, and through the Means Test.

As of 2020, the median household income for a family of one in Arizona is $52,319. That amount increases to $65,713 for a family of two, $71,704 for a family of three, $86,950 for a family of four, and so on. Only spouses and children under 18 are included for purposes of family size. If you and your spouse’s combined income is lower than the corresponding median income, you will qualify for Chapter 7.

The first step of the Means Test is to calculate your (and your spouse’s, if applicable) average income in the six months before your bankruptcy is filed. You will then deduct certain mandatory expenses from your averaged income. If that number is negative, or below a certain threshold based on your family size, you pass the means test and are income-eligible for Chapter 7.

ANSWER:

Unemployment benefits count as income for the purpose of determining your income eligibility for Chapter 7, but your unemployment benefits may not be taken from you by your bankruptcy trustee. For additional information call our Gilbert bankruptcy office today at (602) 598-5099.

ANSWER:

Social security benefits are exempt from Chapter 7 bankruptcy in Gilbert and aren’t included for the purposes of calculating income. A bank account that is only funded by social security benefits is also exempt in bankruptcy.

ANSWER:

Many of our married clients contemplate whether or not they should file a joint petition with their spouses, or proceed with an individual Chapter 7 bankruptcy. You should consult with a bankruptcy attorney before making this decision, especially if you and your spouse have ever resided in a community property state. Your spouse could be held liable for debts that you acquired during the marriage, even if they were in your name alone. If the debts are only discharged as to your name, these creditors could pursue your spouse if you ever were to divorce.

ANSWER:

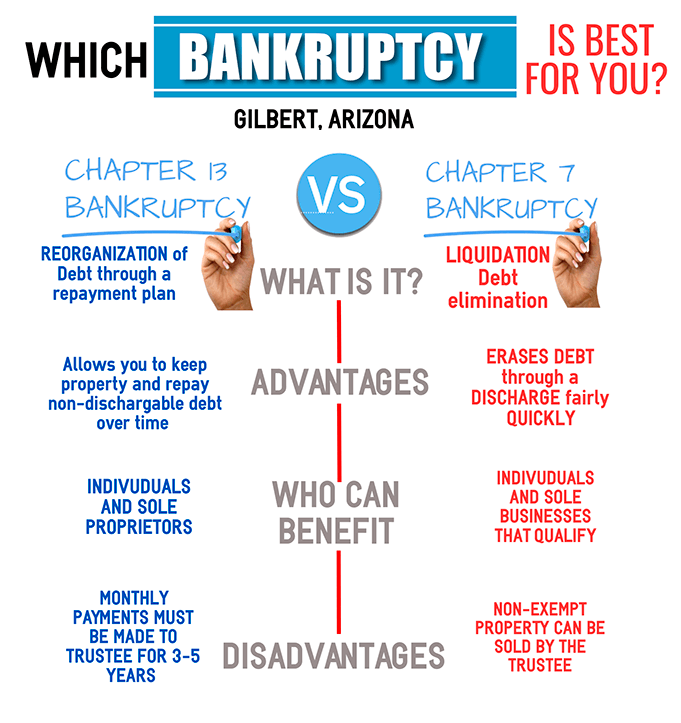

In some situations, you may have the option to file either Chapter 7 or Chapter 13. Chapter 13 may be advantageous if you are behind on payments that are either non-dischargeable or for an asset you wish to keep. For example, child support arrearages aren’t dischargeable in bankruptcy. If you are behind on payments, filing a Chapter 13 bankruptcy in Gilbert may provide a more feasible path to become current while protecting you from collection by your creditors. Or, you may be facing foreclosure on a home your family wishes to keep.

Conversely, a Chapter 7 bankruptcy will only pause a home foreclosure for the few months that the bankruptcy is active, and will resume once your case is discharged if you haven’t become current. Your past-due balance will be spread out in monthly payments over 3-5 years if you choose to resolve it through Chapter 13.

ANSWER:

Everyone who files Chapter 7 bankruptcy in Gilbert must attend a hearing known as a 341 Meeting of Creditors. Therefore, your trustee will be there to ask you questions about your petition, and your creditors have the option to attend and ask questions as well. Also, these 341 hearings are typically quite brief- five or six people may be scheduled within a 30 minute period on each Bankruptcy Trustee’s docket.

ANSWER:

Most Chapter 7 bankruptcy petitioners are able to complete their case within 4-6 months. Your 341 Meeting of Creditors is typically held 30-45 days after your petition is filed, and your case will be eligible for discharge 60 days after that hearing. However, your Gilbert bankruptcy case could take longer if you fail to comply with trustee requests or you miss your 341 Meeting of Creditors. Thus, the process can also be slowed down by external factors, such as upended court procedures due to a pandemic.

ANSWER:

You will be required to take two credit counseling courses as a part of Chapter 7 bankruptcy- one before you file, and one after your 341 Meeting of Creditors. Plus, the credit courses can be taken online, and generally include a brief phone call with a counselor at the end. You will have 60 days after your 341 Meeting of Creditors to take your second course. Each course will cost you around $15-30, and should take you about an hour to complete.

ANSWER:

Your credit cards will be frozen during your bankruptcy by the Automatic Stay. You will likely begin receiving offers for new credit cards once your case has been discharged. Chances are better than not that your current credit cards will close your accounts. However, there are many credit card companies out there that will be eager to work with you after your bankruptcy filing. Additionally, our experienced Gilbert Bankruptcy Attorneys will be ready and willing to assist you with credit questions after filing for bankruptcy.

ANSWER:

The Automatic Stay is a legal provision that goes into effect once your bankruptcy petition is filed. Keep in mind, the Automatic Stay does more than just freeze your credit cards- it also stops your creditors from repossessing your house and vehicle, and from garnishing your wages and bank accounts.

Plus, the Automatic Stay can also prevent evictions and utility shutoffs. The Stay remains effective until your case is either discharged or dismissed. However, your creditors can file a Motion for Relief from the Automatic Stay to request court permission to proceed with collection in spite of your active bankruptcy. It is also vital that your creditor mailing matrix is accurate so that all of your creditors are notified that the Automatic Stay is in place.

The Automatic Stay is a very powerful tool.

ANSWER:

Many forms of property have corresponding exemptions, or asset equity limits for people who file Chapter 7 bankruptcy. Retirement accounts such as 401(k)’s and IRA’s are usually exempt in Chapter 7 bankruptcy. The homestead exemption in Arizona is $150,000. A single filer in Gilbert, Arizona may have a vehicle with up to $6,000 equity, and married filers may either have one car with $12,000 equity or two vehicles with up to $6,000 equity each.

To learn more about the exemptions that an Arizona Chapter 7 Bankruptcy provides, call our Gilbert bankruptcy office today at (602) 598-5099.

ANSWER:

If you see headlines of a company declaring bankruptcy, chances are that they used Chapter 11. There are special provisions for small businesses in Chapter 11, but Chapter 7 may be a better option for some small business owners. Your unsecured debts will be discharged, but the business must cease operations permanently. You can, however, start a business under a new name after your case is discharged. This works best when the business is small, doesn’t heavily rely on its exact name, and the equipment required for its operation is inexpensive.

ANSWER:

Filing Chapter 11 without an attorney is basically unheard of, and less than one percent of Chapter 13 bankruptcies that are filed pro se, or self-represented, are successfully discharged. However, approximately two thirds of Chapter 7 bankruptcies filed without an attorney are discharged. If you are willing to take on that significant risk, your case is simple, and you have a legal background, you may be able to get by self-represented or with the assistance of a document preparer. Otherwise, a qualified bankruptcy attorney can make sure your case runs quickly and smoothly, and that all your assets are protected.

ANSWER:

Many bankruptcy attorneys require you pay both their legal fees and your court filing fees in full before your case is filed. For those struggling with debt, and especially those with a wage garnishment, this can be simply impossible. That’s why our Gilbert bankruptcy attorneys offer Zero Down Payment Plans for our qualified Chapter 7 bankruptcy clients. To learn more about the process and what your payments would be, call today for your free consultation. Speak to an experience Gilbert Debt Relief agent and receive a quote designed to fit your budget, all at no obligation to you. Call our Gilbert bankruptcy office today at (602) 598-5099.

Our Gilbert Bankruptcy Attorneys Picture of Downtown Gilbert, Arizona on a Saturday Night.

The Gilbert bankruptcy Attorneys of My Arizona Lawyers provides residents of Gilbert with experienced, dedicated Gilbert Bankruptcy services . Whereas, each Gilbert bankruptcy and debt-relief case is specific, and our attorneys provide personalized representation in order to achieve the best possible outcome for each case. Thus, as Gilbert residence experience a slow economy, budget cuts, job losses, and emergency life circumstances, many struggle to make ends meet. Additionally, several people in Gilbert and the East Valley are experiencing overwhelming debt. Therefore, bankruptcy, either chapter 7 or chapter 13 bankruptcy can be the solution that many cases need to eliminate or reduce debt, and climb out of a financial crisis. Therefore, Do Not Delay, there is no better time than now to get on the road to financial freedom.

Additionally, while some have a negative view of declaring bankruptcy, thinking of it as a kind of failure, the reality is that bankruptcy was designed to give people struggling with debts a chance to start over. The law provides bankruptcy protection through Chapter 7 and Chapter 13 bankruptcy, afforded under the law to avoid financial ruin. Therefore, sometimes filing for bankruptcy in Gilbert, AZ through experienced bankruptcy services like the bankruptcy attorneys at My AZ Lawyers, Gilbert is the only way to wipe out or organize debt and get a fresh start. Hence, you should call our East Valley bankruptcy team today.

Get Your Finances Back on Track

Also, you should find out how you might be able to get debt relief and start taking back control of your finances by calling My AZ Lawyers today. A Gilbert bankruptcy lawyer may be able to work with you to get you the clean slate that you need. Gilbert bankruptcy services office offers FREE evening and weekend consultations by appointment. Call today (602) 598-5099 and schedule a consult with a Gilbert bankruptcy attorney from our Gilbert bankruptcy services.

Gilbert Bankruptcy Attorneys at My Arizona Lawyers Will Recommend What Chapter of Bankruptcy Is Best For Your Specific Case

Therefore, if you are struggling with seemingly insurmountable debts in Gilbert, Arizona, an experienced bankruptcy lawyer may be able to help you get the debt relief that you need. The Gilbert bankruptcy attorneys at My Arizona Lawyers can evaluate your circumstances and let you know how bankruptcy may be a viable option. The experienced lawyers at My AZ Lawyers can recommend what chapter of bankruptcy might be best for you and can help guide you through the process. Therefore, our Gilbert bankruptcy legal services from our Gilbert debt relief firm are provided with a low fee guarantee and start with a free consultation.

In Arizona, though you technically can file for bankruptcy yourself, it is not recommended. Remember, Filing for bankruptcy can actually be a complicated process. Whereas, failing to get all the details just right can result in severe penalties or loss of property. Therefore, by working with a bankruptcy lawyer, you can ensure that all the paperwork is filed appropriately. Additionally, you are taking advantage of all the opportunities that bankruptcy affords you, such as the possibility of keeping certain assets.

Our Gilbert Bankruptcy Team

Our Gilbert bankruptcy attorneys will make sure that every document is filed completely and correctly. Also, by hiring a competent and experienced bankruptcy attorney in Gilbert, you can be sure that nothing involving your debt-relief case goes overlooked. For some clients, declaring bankruptcy can be stressful and intimidating. However, with our firm’s knowledgeable legal counsel, you can relax and be certain that you are on the road to a brighter financial future. Additionally, our Gilbert bankruptcy attorneys understand the emotional toll that overwhelming debt and bankruptcy can have on a person. Plus, our Gilbert bankruptcy legal team works swiftly and efficiently so that you can get rid of debt and look forward to a brighter financial future.

Gilbert Chapter 7 Bankruptcy Attorney

Chapter 7 bankruptcy in Gilbert, Arizona is also known as liquidation bankruptcy. Also, it is referred as Chapter 7 bankruptcy because assets can and may be used to pay off creditors. Is Chapter 7 the right fit for your financial needs? Furthermore, a means test will determine if you are eligible for Ch 7, and if it is the best way to eliminate debt. Our experienced Gilbert bankruptcy lawyer will help you understand the means test during a consultation with our Gilbert chapter 7 lawyers. Additionally, the moment we file a petition for Chapter 7 bankruptcy, an automatic stay will prevent all collection attempts from creditors. The length of this stay can vary. You should consult your attorney about the terms of a Chapter 7 bankruptcy and its implications in your personal financial situation.

Gilbert Chapter 13 Bankruptcy Lawyer

A Gilbert Chapter 13 bankruptcy is also known as a reorganization bankruptcy. This type of Gilbert bankruptcy is called “Chapter 13” because your debts are reorganized. The Ch 13 allows a payment plan to pay off your creditors over the course of three to five years with your monthly income. Unlike in a Chapter 7 bankruptcy, you will probably be able to keep most, if not all, of your assets. Assets in a chapter 13 are not used to satisfy the claims of your creditors. Additionally, Chapter 13 BK is a consumer bankruptcy that is designed to alleviate the financial burden that our clients carry with them while trying to keep up with their bills. Therefore, our Gilbert bankruptcy attorneys will assist you in every step of the way in the Chapter 13 bankruptcy process.

Bankruptcy Services Gilbert, AZ

Affordable Bankruptcy Attorneys in Gilbert, Arizona

I know what you’re thinking.

“Is This Really a $0 Down Bankruptcy Filing?”

Call (602) 598-5099 today to make sure to qualify.

CALL OUR GILBERT BANKRUPTCY TEAM TODAY – (602) 598-5099

Forget what you think you know about bankruptcy and contact our Gilbert bankruptcy services today. We can help you to find peace of mind and assist you in taking charge of your financial future. Our Gilbert bankruptcy team can put an end to the affect debt has on all aspects of your life: personal, professional, family, and financial. Also, Arizona bankruptcy laws are put in place to give people struggling with debts a helping hand. Gilbert bankruptcy is designed to take away the burden of debt that causes Gilbert residents debt stress. Take the first step today. Call our office to schedule a free consultation and debt evaluation with an experienced Gilbert bankruptcy law attorney — you will be glad you did.

Why Choose Our East Valley Bankruptcy Lawyers?

Trust our experience. Our East Valley bankruptcy team in conjunction with the thousands of successful bankruptcies that we have filed in Pima, Pinal, And Maricopa County make us the logical choice when searching for a bankruptcy lawyer in Gilbert, San Tan, Apache Junction, or anywhere in the East Valley of Phoenix, Arizona. Therefore, if you are seeking a Zero Down Bankruptcy Option or a Same Day bankruptcy filing, contact us right away.

Same Day Bankruptcy Filings in Gilbert, Arizona

Additionally, you should contact our Gilbert Zero Down Bankruptcy office to schedule an appointment with one of our Gilbert debt relief lawyers. Also, if you are in need of immediate debt relief or legal representation and service, our Gilbert bankruptcy firm can help you by obtaining your information and do a same-day filing.

Same day bankruptcy filings are an easy way to avoid a foreclosure or stop a garnishment. Whereas, once a bankruptcy petition is filed the “Automatic Stay” kicks in and halts all collection action against you. Additionally, Same-day bankruptcy filings can prevent creditors from bothering you with collection efforts. So, if interested in finding out more about same day bankruptcy filings, contact us today.

Down Bankruptcy attorney in Gilbert. Zero Down Bankruptcy Attorneys." width="304" height="294" data-lazy-srcset="https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM-200x193.png 200w, https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM-300x290.png 300w, https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM.png 346w" data-lazy-sizes="(max-width: 304px) 100vw, 304px" data-lazy-src="https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM.png"/>

Down Bankruptcy attorney in Gilbert. Zero Down Bankruptcy Attorneys." width="304" height="294" data-lazy-srcset="https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM-200x193.png 200w, https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM-300x290.png 300w, https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM.png 346w" data-lazy-sizes="(max-width: 304px) 100vw, 304px" data-lazy-src="https://myazlawyers.com/wp-content/uploads/2020/02/Screen-Shot-2020-02-23-at-7.45.56-AM.png"/>